KYC in insurance in 2026

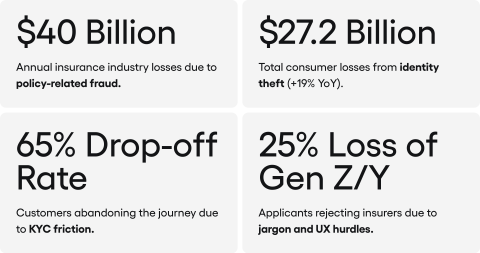

Some 65% of customers abandon a policy purchase when KYC in insurance turns out to be too complicated, according to Capgemini Research Institute. Set that against the threats the industry faces (deepfake attacks up 900%, fraud losses hitting $40 billion a year, per Prove’s “State of Identity 2026”) and the picture is striking. Traditional onboarding creates losses on two fronts: it drives up costs by scaring off honest customers while still letting fraudsters through.

Mobile KYC is the way out. It is the only realistic path to cutting customer acquisition cost (CAC) by 30%, while protecting portfolios against sophisticated digital fraud.

Key takeaways

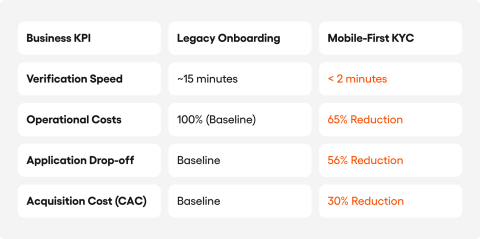

- Full automation of mobile KYC can cut operating costs by 65%, according to Feathery, and shrink verification time from 15 minutes to under 2 minutes, as documented by Decentro. A process that recently required a lengthy agent call or paper forms has been stripped down to an absolute minimum.

- By December 2027, EU insurers will be legally required to accept EUDI Wallet digital wallets under the eIDAS 2.0 regulation. Yet only 4% of firms have taken any real steps, a Bitkom survey reveals. The gap between what regulations demand and actual industry readiness keeps growing.

- Humans correctly spot AI-generated recordings just 40% of the time, warns Prove. Traditional biometrics based solely on facial images is losing its credibility. Gartner predicts 30% of firms will consider it insufficient by 2026. The answer lies in behavioural biometrics, which tracks over 3,000 signals describing how a user interacts with their device, as documented by Facephi and Gartner. The algorithm no longer just checks what you look like. It analyses how you behave, and that is something deepfake technology cannot fake.

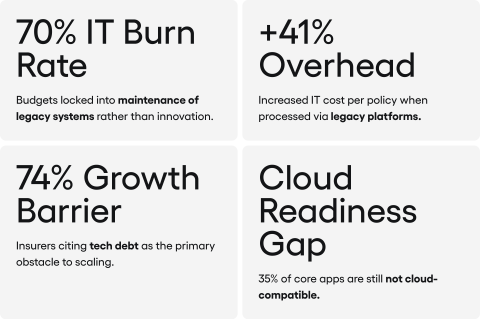

- Insurers spend 70% of their IT budgets maintaining outdated systems, a problem highlighted by Adacta Fintech citing PwC data. The IT cost per policy ends up 41% higher than on modern platforms. Legacy systems slow down every attempt at innovation, including mobile KYC, by raising costs and stretching timelines.

- Within just twelve months, AI use in KYC and AML processes jumped from 42% to 82% as of 2025, a sharp rise recorded by Fenergo. Such a rapid shift signals a widespread move away from manual workflows.

- Automated identity verification platforms (for example, the Noah and Sumsub integration) sped up onboarding by 63% and reduced abandoned applications by 56%, according to Prove. The challenge is tool fragmentation. Automated platforms bring multiple providers together into a single process.

- The insurance market is moving from one-time checks to continuous identity assurance, where a customer’s identity is monitored through on-device biometrics and digital wallets, a trend confirmed by both Prove and Daon. Verification is no longer a one-off gate. It is becoming an invisible process that runs throughout the entire insurance relationship.

- Modern digital platforms generate savings while also lifting revenue by 25% thanks to a fourfold increase in the speed of launching new products, as BCG points out. Mobile KYC therefore opens the door to faster market responsiveness, making it far more than just a budget line item.

What KYC in insurance actually means: definition, process scope and the role of AI agents

In the insurance context, mobile KYC is an integrated process of remotely verifying a customer’s identity on a mobile device. It covers scanning an identity document, biometric verification with a liveness check (confirming there is a real person in front of the camera), screening against sanctions and politically exposed persons databases (AML/PEP), and, increasingly, accepting the European EUDI Wallet. A McKinsey report, “The Future of AI in the Insurance Industry” (July 2025), describes a future where nearly all onboarding functions could be handled by multi-agent AI systems. Specialised agents work in parallel on application intake, risk profiling, pricing and regulatory compliance.

The scale of the problem that mobile KYC solves is well documented. Capgemini analysts, in their “Insurance Top Trends 2026” report (January 2026), confirm that burdensome data collection is the main reason customers drop out. A joint Capgemini and LIMRA report (“World Life Insurance Report 2026”, September 2025) sharpens that finding: one in four consumers under 40 turns down life insurance because of confusing processes and jargon. Only 16% of insurers offer an integrated service blending digital channels with advice, though 67% of younger customers expect exactly that.

Data published by Javelin Strategy (“2025 Identity Fraud Study”) confirms the fraud threat. Consumer losses from identity theft reached $27.2 billion in 2024, up 19% year on year, with new account fraud growing fastest. Mobile KYC therefore serves a dual purpose: it holds on to impatient customers and guards against fraud at the same time.

6 technology trends driving KYC in insurance (2026)

Recent reports point to six main technology trends shaping the mobile KYC market in insurance in 2026. Each one can shift the market on its own, but it is their combined presence and mutual reinforcement that creates the real effect.

Behavioural biometrics: 3,000 signals a deepfake cannot copy

Behavioural biometrics is probably the most underrated trend in mobile KYC. Solutions like those from Facephi (2025) analyse over 3,000 behavioural signals, from typing speed and rhythm through device movement patterns to finger pressure on the screen, building a unique digital profile for each user. The technology already works and handles challenges that traditional biometrics simply cannot.

The Prove “State of Identity 2026” report lays bare the problem. Around 70% of organisations do not check behavioural patterns, and people correctly identify deepfakes only 40% of the time. Since humans cannot tell a real face from a synthetic one, Gartner forecasts that by 2026, 30% of enterprises will stop relying on facial recognition alone, adding behavioural analysis and device identification.

The behavioural biometrics market is expected to reach $7.37 billion by 2030 (Zion Market Research), while biometrics applications in insurance could hit $17.6 billion by 2033, according to Ethos Risk (November 2025).

EUDI Wallet and eIDAS 2.0: digital wallets in insurance onboarding

The eIDAS 2.0 regulation (EU 2024/1183) sets a precise timeline. All EU member states must deploy EUDI wallets by December 2026, and from December 2027 insurers will have to accept them for identity verification. Gartner backs this trend, estimating 500 million people will regularly use digital wallets by end of 2026.

This shift will reshape how data is collected. Selective disclosure means an insurer could confirm a customer is over 25 without ever seeing their exact date of birth.

Industry readiness looks worrying, though. A Bitkom survey from Germany (November 2025) shows 82% of companies intend to use the EUDI Wallet, yet just 4% have taken real steps. Late adoption will pile up work right before the deadline, meaning wasted budgets and unavoidable technology compromises.

AI in document verification: 95–99% accuracy and no more delays

Market data shows just how mature document verification algorithms have become. Shift Technology already reports 95–99% extraction and classification accuracy for printed documents. Advanced multimodal models examined by RGA allow text, image and video analysis to be combined into a single workflow. Accenture estimates that AI lets insurers process 100% of incoming requests and double the number of applications reaching the pricing stage by cutting out broker-underwriter back-and-forth.

An analysis by CheckFile.ai across 25,000 files (2025) shows that 42% of onboarding delays in financial services come from missing or expired documents. Every such delay pushes up abandonment rates, making automatic gap detection a vital part of the sales process.

Liveness detection: how to check there is a real person behind the camera

Liveness detection checks whether the person in front of the camera is a living human, not a photo, recording or AI-generated animation. The technology has evolved from active challenges (blinking, head turns) to passive methods based on a single photo. HyperVerge achieved ISO 30107/3 Level 2 compliance with single-photo verification, training on 850 million completed checks.

Data cited by OLOID shows that active liveness testing (Sumsub) reduces fraud by up to 91%, with particular effectiveness against deepfakes. Veridas, ranked fifth in the NIST 2026 benchmark at N = 12 million, uses injection attack detection and a MAD (Massive Attack Detection) system for real-time pattern analysis.

Dropping active tests in favour of passive methods directly improves user experience. Removing unnatural movements in front of the camera speeds things up and reduces frustration, which translates straight into higher sales conversion.

Automated verification orchestration platforms

Automated identity verification orchestration platforms bring multiple providers into a single process. DevCode Identity (February 2026) integrates over 200 KYC and identity providers. The Noah and Sumsub integration sped up onboarding by 63%, cut abandoned applications by 56% and nearly doubled monthly KYC throughput, as documented by Prove.

In its 2026 outlook, Accenture describes “innovation fabrics”: architectural layers built from reusable business components managed by AI, allowing changes without rewriting the core system. An insurer could plug in a new biometrics provider or change the verification path for a specific customer segment without disrupting the main platform.

Continuous identity assurance across the policy lifecycle

The one-and-done verification model is giving way to continuous identity assurance. As Prove puts it, a single identity check is no longer enough; continuous assurance across the full customer lifecycle is becoming the standard. Daon (December 2025) forecasts that 2026 will be defined by five key technologies: wallets with selective disclosure, anti-deepfake systems, on-device biometrics, continuous employment verification, and KYA (Know Your Agent) frameworks for authorising autonomous AI agents acting on a user’s behalf.

Continuous identity assurance shifts the focus from a one-time check at policy purchase to ongoing session monitoring. This catches account takeovers, unauthorised data changes and fraud attempts in real time, at the moment an incident happens rather than weeks later at the claims stage.

Market data and ROI: what KYC in insurance costs and saves

Size and growth of the global identity verification (IDV) market

The global identity verification (IDV) market was valued at $14.34 billion in 2025, forecast to reach $29.32 billion by 2030 at a CAGR of 15.4%. The segment covering KYC, business verification (KYB) and onboarding makes up 43.2% of the market, according to MarketsandMarkets. The biometric identity verification market stands at $8.88 billion in 2025 and is set to grow to $17.81 billion by 2030 at a CAGR of 14.9%, the same research firm reports.

A narrower slice focuses directly on insurance. The electronic KYC market in insurance was estimated at $120.87 million in 2024, projected to reach $261.18 million by 2032, per MarketsandData. The digital onboarding market as a whole is growing from $2.5 billion in 2023 to a projected $9.8 billion by 2032 at a CAGR of 16.2%, per Dataintelo.

Onboarding time: from 15 minutes to under 2 minutes with automation

Real-world deployments provide strong evidence. InsurTech BimaPay, working with Decentro (2025), cut onboarding from 15 minutes to under 2 minutes, an 87% reduction. Across the wider industry, median KYC verification time fell by 43%, from 4 minutes 50 seconds to 2 minutes 44 seconds, in a Shufti benchmark for the BFSI sector (January 2024 to March 2025).

Conversion and operating costs after digital KYC deployment

Digital onboarding raises the rate of completed policy purchases by 40–60%. Full process automation adds another 11 percentage points to conversion, as documented by Shufti.

Three key areas for cost savings stand out. Onboarding automation delivers around 65% savings in operations, according to Feathery. Broader digitalisation can cut an insurer’s fixed costs by nearly 40%, Bain forecasts. EY highlights life insurance, where straight-through processing (STP) shortens policy issuance by 50% and frees up 40% of staff capacity.

Customer acquisition cost (CAC) in insurance and the impact of going digital

Customer acquisition costs in insurance are among the highest of any industry, averaging $500 to $900 per customer and reaching $1,200 for agent-sold life insurance. Winning a new customer costs seven to nine times more than retaining an existing one, EasySend notes. Every percentage point recovered at onboarding is pure profit.

Digital strategies can reduce CAC by up to 30%, Ringy confirms, while deep AI integration cuts onboarding costs by nearly half, as McKinsey estimates. But these are not just savings. Modern platforms boost revenue by 25% and speed up product launches fourfold, BCG highlights. That combination of lower costs and higher sales creates a financial effect traditional methods cannot match.

AI adoption in KYC and AML: from 42% to 82% in one year

A Fenergo survey of 600 decision-makers confirms the problem: seven in ten firms lose clients because onboarding is too complicated. AML and KYC operating costs, averaging $72.9 million a year, have forced the industry into rapid digitalisation. AI use in these processes nearly doubled in a single year, reaching 82%. Not having AI in place is no longer a missed optimisation; it is a real risk of falling behind.

5 barriers to KYC deployment in insurance, and how to overcome them

Mobile KYC deployment typically runs into five main obstacles. None is a permanent blocker, as long as the company manages risk and technology carefully at each stage.

Fragmented AML/CFT regulations across Europe and the US

Regulatory fragmentation in the AML/CFT space remains a serious challenge. In 2025, Europe has eIDAS 2.0, the new AMLR regulation (EU 2024/1624, effective July 2027), the 6AMLD directive with an expanded catalogue of predicate offences, and AMLA, which started operations in July 2025. The US alone introduced eight new state privacy laws in 2025, as documented by White & Case.

Operating across multiple markets means adapting to often conflicting requirements under GDPR, HIPAA and CCPA. Informatica’s experts point to “regulation fragmentation” that makes standardising processes very difficult. The risk is measurable: AML fines worldwide hit $4.6 billion in 2024, as Fenergo reports.

Legacy systems: when 70% of the IT budget goes to keeping outdated platforms alive

Outdated IT systems are probably the biggest, yet least discussed, barrier to change. A 2025 Adacta Fintech survey found that 46.4% of insurers see inflexibility as their main limitation, 45.5% struggle with integrating new technologies, and 44.5% point to high maintenance costs. Data cited by Adacta Fintech (via PwC) shows insurers spend 70% of IT budgets on old systems, with the IT cost per policy 41% higher on legacy platforms.

A HFS/Sutherland report (2025) confirms the scale: 74% of insurers admit legacy systems hold back growth, yet only 28% have a proper modernisation plan. BCG reports that European and North American insurers will spend a combined $17 billion on core IT modernisation from 2024 to 2026. Despite these investments, 35% of applications are still not cloud-ready, and only 36% of firms use a centralised customer data repository.

Data privacy and building digital trust with customers

The average cost of a data breach stood at $4.88 million in 2024. California enacted the Insurance Consumer Privacy Protection Act (SB 354, 2025), and the FTC took action against GM/OnStar for collecting and selling driver geolocation data used to set insurance rates without consent. NAIC is updating the Insurance Data Security Model Law, with a full draft expected in early 2026.

A Capgemini report flags an interesting trend: 60% of respondents are willing to share data if it results in a better-tailored policy. This opens the door to transparent KYC procedures built on reciprocity. A customer knowingly shares information, understands its purpose and the value of the offer they get in return. That builds loyalty more effectively than older approaches.

Cross-border compliance and differences in EUDI Wallet implementation

Despite legal changes, a single cross-border identity verification system is still fiction. The Payments Association (2025) admits a unified standard is still a long way off. Though the EUDI Wallet is meant to be the answer, each of the 27 member states is implementing it on its own terms, forcing companies to prepare separately for each market, as Signaturit highlights. An onboarding flow that works perfectly in one country may prove useless just across the border.

Digital exclusion: who gets left out by mobile-only onboarding

Digital exclusion affects an estimated 627 million people worldwide. A Keynova survey (Q4 2025) of the 12 largest US auto and property insurers, cited by Insurify, found that two-thirds do not offer a clear digital channel for reporting accessibility issues.

The inequalities run along geographic, socioeconomic and age lines. In the US, households earning under $30,000 own smartphones at 79%, compared to 98% among those earning over $100,000 (Pew Research), as cited by EasySend. That 19-point gap is a reminder: a system built only on mobile channels shuts out a significant share of the population, often the very people who need insurance protection the most.

KYC deployment strategies in insurance: recommendations from McKinsey, BCG, Bain and others

McKinsey: six “signature moves” in AI transformation

McKinsey (July 2025) sets out six “signature moves” for AI transformation in insurance, each directly relevant to mobile KYC. These include aligning leadership around a business-led AI roadmap, building an internal digital team (70–80% hired internally), adopting a scalable operating model, using technology to speed up innovation, embedding data in all processes, and investing in change management.

The firm’s view is clear: instead of relying on outside vendors, insurers should build their own teams under strong board leadership. The whole organisation must shift to a data-driven model capable of scaling innovation quickly. Time for stopgap solutions is over. Only a fully integrated onboarding process, combining identity verification with payments and digital signatures, delivers a visible competitive edge today.

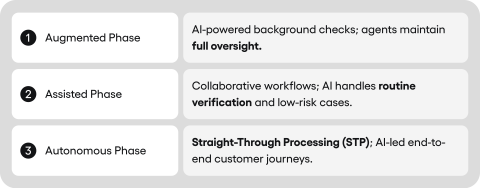

BCG: three waves of AI in distribution, from agent support to full autonomy

According to BCG’s 2026 projections, automation is heading towards full system autonomy, which could cut back-office and onboarding headcount by as much as half. The recommendation is straightforward: routine processes with no emotional dimension should move to direct system-to-system communication. The customer’s role is reduced to the bare minimum, which radically speeds up the entire operation.

Bain: five initiatives for KYC process optimisation

Bain (“Bridging the Protection Gap”, March 2025) estimates AI’s potential at 10–15% revenue growth, up to 30% operational savings, and 30–50% claims leakage reduction in the P&C segment. For KYC, Bain recommends five initiatives: identify only the data you actually need; simplify processes; use external KYC providers; standardise data structures; set up continuous monitoring with a feedback loop. Each targets a different part of the problem, but together they form a strategy that simplifies operations while tightening control.

Oliver Wyman: data control and onboarding live in 6–9 months

Oliver Wyman (February 2026) argues that data control and AI system localisation are project foundations, not afterthoughts. Information security must shape the architecture from the very start. Their Edge platform offers ready-made onboarding processes that can go live in 6–9 months, proving that fast deployment is possible. Rather than building everything from scratch over years, it is better to rely on proven components.

Forrester and Deloitte: deepfakes, verification costs and AI maturity among insurers

As Forrester (2025) sees it, mobile KYC progress is blocked by four factors: legacy biometrics vulnerable to deepfakes, low system efficiency, regulatory paralysis, and pricing pressure forcing commercial model changes. The gap between ambition and reality is confirmed by a December Deloitte report: even though three-quarters of insurers use AI, for most it remains a promising prototype. Moving from concept to production is the sector’s biggest challenge right now.

The future of KYC in insurance: from digital wallets to machine identities (2027–2030)

From one-time verification to continuous identity assurance

The future of mobile KYC goes far beyond efficient document scanning. The industry is moving from one-off checks towards continuous identity assurance, setting a new security standard, a trend backed by Prove and Daon. The scale of this shift is best shown by the decentralised identity (SSI) market. DataM Intelligence estimates it will grow from $1.3 billion in 2024 to nearly $45 billion by 2032. A 35-fold jump in eight years proves SSI is leaving the lab, and the EUDI Wallet is becoming its first mass deployment in Europe.

A digital wallet turns the multi-step policy purchase into an instant transaction. The insurer receives a complete set of verified data, from identity to driving history, without any manual checking. This “instant issuance” model, examined by Doxee among others, is no longer a curiosity. It is becoming a real strategic goal for modern insurers.

Know Your Agent (KYA): are insurance systems ready for AI customers?

Mobile KYC is entering a phase of verifying AI agents that are starting to dominate the digital ecosystem. Machine identities may outnumber human ones by a factor of 144. Standards like KYA are becoming a necessity to safely handle transactions started by bots buying policies on behalf of customers, as the Daon report points out.

For insurers, this means a triple verification: the customer, their digital representative, and the code integrity of that agent. As the Swiss Re Institute warns, this paradigm shift creates new ground for fraud and disputes over responsibility for AI decisions, while amplifying systemic risk from the industry’s dependence on a narrow group of AI infrastructure providers.

Insurers that build solid mobile KYC foundations now, bringing together behavioural biometrics, automated verification platforms, EUDI Wallet readiness and AI, will be best positioned for what comes next.

Speed of change as a competitive advantage

The most important takeaway? The time for experiments is over. eIDAS 2.0 regulations will force insurers to accept digital wallets by 2027. While most of the market jumped to AI in a single year (42% to 82%, as Fenergo documents), laggards still burn 70% of their budget keeping old systems alive, per Adacta Fintech. The result? They lose 65% of customers before those customers even see an offer, warns Capgemini. The real threat is not a lack of tools. It is the chaos that comes from buying dozens of small, disjointed solutions.

Frequently Asked Questions (FAQ)

How do insurance companies secure financial transactions against financial fraud?

Insurance companies secure financial transactions by implementing automated mobile know your customer platforms. By analyzing over 3,000 behavioral signals and utilizing liveness detection, the insurance sector can effectively prevent fraud, combat money laundering, and protect financial institutions from sophisticated financial crime and costly deepfake attacks.

Why is a customer identification program vital for anti money laundering and customer due diligence?

A digital customer identification program automates customer due diligence, helping the insurance industry achieve strict kyc compliance. This streamlined kyc process allows an insurance company verify users instantly, successfully managing aml risk and identifying money laundering or terrorist financing threats faster than outdated offline kyc methods relying on physical documents.

How does digital onboarding improve customer experience while trying to ensure compliance?

Digital onboarding enhances the customer experience by reducing verification time from 15 minutes to under 2 minutes. This rapid online kyc allows insurance companies to seamlessly ensure compliance with regulatory requirements, monitor suspicious activities, and assess potential risks, which prevents honest customers from abandoning their insurance policies during signup.

What serves as valid identity proof, and how do adverse media and adverse media screening help?

Modern identity proof relies on scanned ID documents, liveness checks, and the upcoming EUDI digital wallets. Concurrently, checking for adverse media through automated adverse media screening allows insurance firms to evaluate associated risks and aml compliance. These are key components to prevent financial crime and block money laundering attempts.

How does anti money laundering aml manage aml risk through continuous monitoring?

Anti money laundering aml is shifting from one-off checks to continuous identity assurance. This ongoing risk management tracks customer information and behavioral biometrics during the entire lifecycle of insurance policies. It enables the insurance sector to instantly detect suspicious activities, lower aml risk, and halt money laundering in real-time.

What are the regulatory requirements for the insurance sector regarding digital wallets?

By December 2027, the eIDAS 2.0 regulation mandates that the insurance sector must accept EUDI digital wallets. This shift will streamline customer relationships and financial transactions by allowing insurance companies to verify data through selective disclosure, significantly upgrading regulatory compliance and protecting the business from unnecessary financial losses.

How do automated verification platforms impact the operational efficiency of financial institutions?

Automated platforms drastically boost operational efficiency by consolidating multiple providers into a single, seamless kyc process. This integration helps financial institutions process required documents accurately via machine learning, conduct thorough risk assessment, eliminate missing paperwork delays, and quickly spot money launderers before they can initiate fraudulent claims.

Why are legacy IT systems a barrier to implementing an effective online kyc process?

Legacy systems consume 70% of IT budgets for maintenance, making the cost per policy 41% higher than on modern platforms. These outdated systems hinder insurance companies from deploying agile online kyc tools, completing proper customer due diligence, and efficiently analyzing risk factors required by strict governing bodies and regulatory standards.

This blog post was created by our team of experts specialising in AI Governance, Web Development, Mobile Development, Technical Consultancy, and Digital Product Design. Our goal is to provide educational value and insights without marketing intent.